Know Your Company Exit Options

March 15, 2011

One of the most important strategic decisions that start-up companies make is planning how they will make their exit. After all, that decision will allow a company and its founders to work toward a common end goal: a successful, lucrative, and painless market departure.

So when is a good time for a startup company to begin planning its exit strategy?

Truthfully, it’s never too early to start. It’s important to spend time learning about your potential exit options — regardless of when you’re planning for that exit to actually occur — because it can drastically influence your company’s product development, IT, personnel, and product positioning decisions.

In turn, those decisions can also affect the mergers and acquisitions appeal of your firm. Suitors place a

premium on companies that don’t have major software or platform integration issues, have a similar company culture to their own, and foster an environment that will make it easy to integrate their IT infrastructure and product lineups.

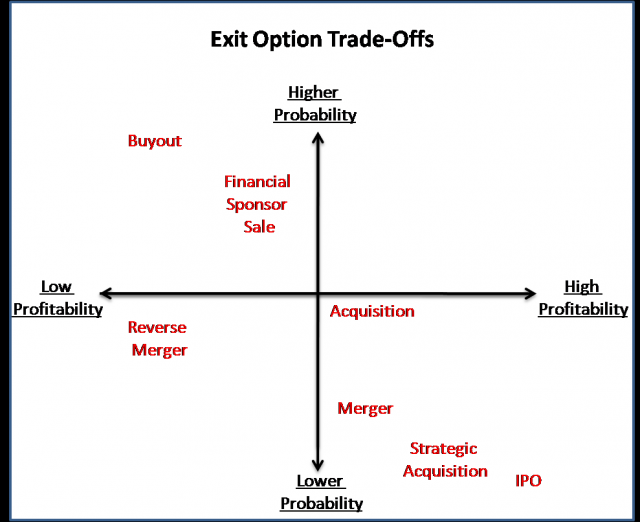

If you haven’t started thinking about those things and their relationship to your exit strategy yet, it might be time to get started. The first step is to identify the various exit avenues.

Here are the most common ones that startup companies can consider:

Initial Public Offering (IPO)

If successful, an Initial Public Offering will yield the biggest dollar payout of any exit strategy. However, it is very expensive to facilitate an IPO and you can easily spend a half million dollars on attorneys and accountants — without any guarantee that the price attained through an IPO will be a profitable one.

The reality is that there were only 96 IPOs in the United States last year and a mere 41 the year before that. So the probability of exiting this way is very low. In the technology sector, market estimates indicate that only 0.01 percent of technology companies successfully exit the market via an IPO. And, while IPO market activity has been on the rise in the last year (compared to 2007 and 2008 levels), it’s still a fraction of what was seen in the mid-90s.

Strategic Acquisition

In this option, you would sell your company to a strategic acquirer, who pays a huge premium for your business (typically greater than five times the revenues of the previous 12 months). Strategic acquisitions are typically driven by one (or both) of the following two criteria:

- A company has developed and patented game-changing technology that would significantly accelerate the acquirer’s business strategy.

- The risk of a competitor acquiring a startup’s technology is too high for the strategic acquirer to take.

If your company is purchased by a strategic acquirer, it’s the second most profitable exit strategy. But similar to an IPO, it’s extremely rare for a technology company to exit via strategic acquisition. Classic examples of this scenario include Google’s acquisition of YouTube and Amazon’s acquisition of Zappos.

Acquisition

Acquisition

Here, you would sell your company to a non-strategic acquirer who pays a smaller premium — market value or slightly under market value to acquire your business. This method is tied for the third most profitable and it’s becoming an increasingly popular exit strategy.

PricewaterhouseCoopers reported that there were 4,251 global M&A transactions in 2010 and Reuters reported that more than 400 of those deals were venture backed acquisition exits, the largest number since records began in 1985.

Merger

In this scenario, you make a deal with another company to combine all — or part — of your own business with theirs in return for stock (or stock and cash) in a newly formed company or division.

Some well known merger examples include Google’s merger with Admob and Southwest’s merger with AirTran. Mergers are tied with Acquisitions as the third most profitable exit strategy. One downside to this method is that it does not necessarily liquidate your business. But it does provide you with marketable stock that could be sold. Merger exits are not as common as acquisition exits.

Buyout

With a buyout, you sell your company to an employee or someone outside of the business via a private sales transaction. The price that the buyer pays can vary significantly (from above to below market value) depending on the circumstances.

Reverse Merger

In this scenario, your company acquires a public shell company that is no longer active, but remains listed on a public stock exchange. By doing that, your company converts itself into a public company with stock that it can sell on the open market. That allows you to flip some or all of your equity into cash.

From a structural perspective, reverse mergers are cheap, fast, and relatively easy to execute. However, it’s also extremely unlikely that a company will be able to attract significant market interest or high valuations via the reverse merger route if it’s performance is not strong enough to justify an IPO, strategic acquisition, or merger.

Another downside of reverse mergers is that the newly formed company handcuffs itself with additional regulatory compliance responsibilities that will drive up its overall operational costs and decrease its competitiveness in the market. Thus, this is generally an ill-advised strategy.

Financial Sponsor Sale

One of the more common exit strategies is a financial sale to a private equity or holding company that plans to restructure the company or re-position it to improve its performance and prepare it for a strategic acquisition or IPO. Most financial buyers will pay between one to three times the previous 12 months of revenue, which makes it a particularly attractive exit strategy.

Now that you know the potential options, you should be ready to start thinking about — and planning for — your company’s exit strategy.

It doesn’t have to be a painful process. If you plan for it long in advance of the exit and understand which avenue makes the most sense for your business, the actual exit can be relatively simple. But for that to be the case, you need to understand your exit options first and then harmonize your business’s overall strategy with the option you choose.