The CEO Imperative: Build Your Operational Control Panel

October 13, 2010

As a company progresses from the start-up to the expansion stage, one of the most important things it can do is change the way it thinks about its business.

Start-up CEOs typically make management decisions based on a gut feeling or a practical sense of their business. Meanwhile, financial planning in those same companies can often be based on cash-in, cash-out accounting. Neither of those approaches at the start-up stage are incorrect necessarily. But after raising expansion capital with the goal of growing the business, CEOs need to turn their attention to economic models that will help them do that.

The closest analogy is what a pilot uses to fly a Cessna versus a Boeing 777. A Cessna pilot relies primarily on looking out the cockpit and “feeling” the plane, with occasional glimpses of a basic control panel to validate his sensory inputs. A 777 pilot almost completely relies on his control panel (his operational dashboards), his co-pilot (CFO), his auto-pilot (COO?), and his crew (senior management team).

I’ve written quite a bit about capital efficient growth before (What is a Profitable Distribution Model and The Ideal Path to Expansion Stage Growth). At OpenView Venture Partners, building financial and operational dashboards is one of the first things we do to help our expansion stage CEOs.

The goal of those dashboards is to provide the CEOs with a high level summary of their key operational metrics. Ultimately, it also allows them to make decisions based less on gut feelings and more on quantifiable data, putting their companies on track to grow and expand.

Our OpenView Labs team has developed a high level dashboard that covers the basic financial and operating metrics of our portfolio companies. Below is a rundown of the key features of that dashboard, along with some of the questions I ask myself as I review data.

Note that the numbers represented in these charts are totally fictitious, to protect the innocent.

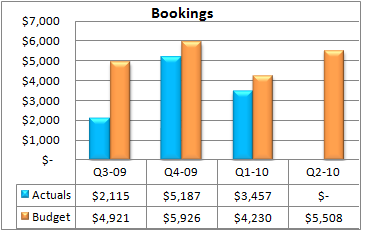

Bookings

What’s the definition of a booking? That can vary depending on the company, but it can be the value of the first month of a monthly subscription or it can be the first year of a three year contract with annual invoicing. Whichever it is for your company, my recommendation is to stay within a year of booking value. In other words, don’t book multi-year deals, even if you sell the occasional three year contract.

Accuracy in budgeting and forecasting is also an absolute fundamental need in software companies. Executives and management teams must always be aware of forecasting hits and misses. That, of course, means that CEOs and their management teams need to gauge the productivity of sales reps, understand how marketing dollars translate to future bookings, and forecast the effect of seasonality on the business.

Accuracy in budgeting and forecasting is also an absolute fundamental need in software companies. Executives and management teams must always be aware of forecasting hits and misses. That, of course, means that CEOs and their management teams need to gauge the productivity of sales reps, understand how marketing dollars translate to future bookings, and forecast the effect of seasonality on the business.

If a missed forecast affects bookings, companies should ask themselves if a forecast revision is necessary for the following quarter.

Revenue

Depending on the type of licensing, revenue adds another dimension to the operational perspective that you don’t get from bookings. ![]()

Some questions to consider:

Are we set up with proper GAAP revenue recognition? What are the steps we need to take to ensure that we are?

Where are the budgeted revenue gaps coming from? Are we seeing a change in balance between revenue and services or a shift in how our sales contracts are being executed?

Renewal and Upsell

Expansion stage companies tend to neglect two sales categories: renewals and upsells. It’s not because those companies aren’t interested in them. Rather, it has much more to do with expansion stage companies being exceptionally focused on new customer acquisition.

![]() However, the opportunity to retain and sell more to customers is a huge, untapped source of lower cost revenue. When you examine your renewal and upsell potential, it’s important to consider a few key questions:

However, the opportunity to retain and sell more to customers is a huge, untapped source of lower cost revenue. When you examine your renewal and upsell potential, it’s important to consider a few key questions:

- What is my current renewal rate and why is it not 100 percent? What is the profile of customers that have churned, how do we classify them, and what are the reasons for them churning?

- Are we selling to the right customer profile? What is the profile of our renewals? How do we find more of them?

- Is our product meeting expectations? Do we need to offer a training program for our customers to be sure they understand the best use of our product?

- What is our upsell rate to current customers and how do we increase it? Do we have an active account management process and sales reps dedicated to upselling existing customers?

If your renewal or upsell rate is low, consider putting a “lost customer” calling program in place to survey your non-renewals. The answers you get will likely help keep those churning customers in the future.

Distribution Economics

When it comes to the economics of scaling an expansion stage company, paying attention to the profitability of a distribution model is extremely important.

The goal of a profitable distribution model is quite simple to conceptualize, but quite complex to achieve and maintain through the expansion stage. As you prepare and analyze yours, you should ask these questions:

The goal of a profitable distribution model is quite simple to conceptualize, but quite complex to achieve and maintain through the expansion stage. As you prepare and analyze yours, you should ask these questions:

- What are our priorities relative to the profitability of our distribution model? What is our growth strategy in connection to available capital and what operational steps can we take to attain economics?

- How do variables like gross margin, bookings, and sales and marketing costs impact the distribution model?

- What should be our priority going forward? Do we need to explore sales and marketing support to help reach our goals?

Now let’s talk about cash. One of the biggest drivers of cash consumption in today’s software companies is the licensing model that they use. Companies that offer a perpetual licensing model can look forward to receiving from customers the bulk of the related revenue/cash in the first year of sale. Which means that cash comes in soon after a sale is booked. This allows the company to recover the majority of the cost of sale and delivery in the first year.

Subsequent year cash flows are more limited to the traditional 20-25% maintenance revenue. On the cost side, these companies typically have a higher cost of new customer acquisition (keep in mind, I’m mostly a B2B guy).

Subscription-based companies have a different cash profile. The lifetime revenue of a customer is spread over 1-5 years in equal license installments. This means that the initial cash received in the first year is a fraction of that of perpetual license companies. On the other hand, if the company can recover its costs in the first 12-24 months, incoming cash after that is pure profit that can fund perpetual growth. The downside is that early stage companies will have to figure out how to make do with less cash in the early years. This is especially so in the case of monthly subscriptions, where the cash comes in monthly, not in quarterly or annual installments.

A few of our portfolio companies actually used perpetual licensing in the start-up years, and shifted to subscriptions (or a hybrid) at the expansion stage.

Operating Cash Flow

The first dashboard looks at the operating cash flow of the company. The key questions to ask here are:

- What is our budget for operating cash flow? What are the assumptions we are using in developing our cash budget? Do we have a good handle on our ability to forecast cash consumption? What is the impact of our licensing, and how do we ensure that the sales team is selling the right types of licenses to support optimal bookings and cash flow?

- With this budget, how far will our cash last? What is the “right” amount of cash burn or cash generation that we should be aiming for? How does that fit with the long term aspirations of the company?

- What are the top drivers of our cash consumption and how should we manage them?

- Why are we missing our cash forecast, and should we re-forecast the remaining quarters?

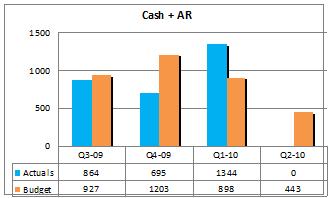

Cash and Accounts Receivables

The combination of cash and A/R gives a high level view of the overall cash position of the company. As the company grows, and with it the A/R account, access to growth capital expands though A/R-based bank financing.

- What is the health of our cash and A/R position? Do we have a good balance between the two?

- Why are we missing our budget, and is our forecast any better? Should we adjust the forecast and the balance between the two?

- What is driving our expanding A/R line and should we be driving it down (more on this in the DSO dashboard)?

- Is our A/R line providing us the option to obtain bank financing? Should we use it?

Days Sales Outstanding

“Days Sales Outstanding is a calculation used by a company to estimate their average collection period. A ![]() low number of days indicates that the company collects its outstanding receivables quickly. DSO figure is an index of the relationship between outstanding receivables and sales achieved over a given period. The DSO analysis provides general information about the number of days on average that customers take to pay invoices.” Wikipedia

low number of days indicates that the company collects its outstanding receivables quickly. DSO figure is an index of the relationship between outstanding receivables and sales achieved over a given period. The DSO analysis provides general information about the number of days on average that customers take to pay invoices.” Wikipedia

- Do we have a strong collections policy and process? Do we have a robust communication process with customers to support collections? Are we allocating enough staff and priority to collections? Is our collections staff aggressive enough in pursuing collections? Are we not being clear at the point of sale what the customer should expect in invoicing?

- What are the drivers to a high DSO number? Are we acquiring customers that we shouldn’t? Are customers not being on-boarded properly, leaving them dis-satisfied? Is our issue with overseas customers? Large or small?

- Are we leveraging various communication channels with customers to alert of late payments (e.g. sales account management, customer service)?